CEMENT SECTOR: FRAGILE RECOVERY

The Indian cement industry, world’s second-largest producer after China, plays an important role in India’s economic growth as it contributes majorly to construction and infrastructure sector. However, contrary to expectations at the start of 2013, the cement industry has not shown any significant signs of revival so far. Marred by weak demand, the overall growth in cement production has fallen to 5.6% in FY13 as compared to 6.7% in FY12.

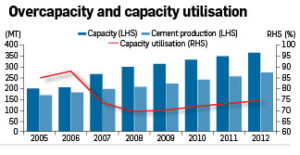

CAPACITY UTILISATION: CONSTRAINED BY SUBDUED DEMAND

CAPACITY UTILISATION: CONSTRAINED BY SUBDUED DEMAND

At present, installed capacity stands at 330 million tonnes. Because of the stabilisation in demand, which was already expected, capacity utilisations was reported at around 71% in FY12. 2013 may observe a decline in the pace of capacity addition, as Indian cement industry already had major capacity additions during FY08-FY11. The growth in capacity additions is expected to be same as FY12, at 5%.

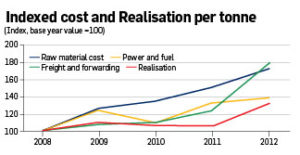

HIGHER INPUT COSTS AND PRICING PRESSURE

HIGHER INPUT COSTS AND PRICING PRESSURE

With the moderation to be expected in demand vis-a-vis the demand surge reported in FY2012, the cement sector’s realisation is likely to see a fall by 5%-10% yoy in 2013. On the cost side, a matter of concern might be increase in freight cost, which accounts for 17%-27% of cost of production, as it has gone up substantially from FY10-FY12. The chief reasons driving the increase are spurring diesel prices and high rate of inflation. Also, power and fuel costs have increased considerably from FY08-FY12.

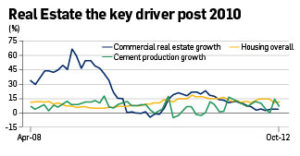

THE KEY DRIVER: REAL ESTATE SECTOR

THE KEY DRIVER: REAL ESTATE SECTOR

Prior to 2010, the cement demand was mainly driven by infrastructure, roads and construction sector. Post 2010 the demand is largely driven by the housing and commercial real estate sector. However, rising inflation rate coupled with contraction in growth has adversely affected the infrastructure projects across India in 2012, due to which it is expected that the cement growth may remain in the range of 5%-8% in 2013.