Last month, on March 25, 2013, Cyprus became the first country in the troubled eurozone to impose capital controls since the formation of the single currency union in 1999. Clearly, it wasn’t an easy call for Nicos Anastasiades, the Cypriot President, but then he had no choice. The country urgently needed a 17 billion euro bailout to recapitalise its banking system (the island nation’s banks have suffered major losses from the write-down of Greece’s government debt and from non-performing loans made in Greece), failing which the entire financial system might collapse.

Although the negotiations with the European Union (EU), European Central Bank (ECB) and International Monetary Fund (IMF), which lasted over 12 hours, did cost him the island’s second-largest bank – Laiki Bank – and an unprecedented raid on deposits over 100,000 euros (accounts with more than 100,000 euros, face losses of 4.2 billion euros), he seemed happy as he had prevented Cyprus from becoming the first country forced out of the single currency union.

The Mediterranean island, which represents just 0.2% of the eurozone economy, is the fourth economy in the single currency area to be completely bailed out after Ireland, Portugal and Greece. But unlike previous bailouts, a majority of the country’s financing needs are supposed to be met by its oversized banking sector – in particular by depositors. While the the “troika” has agreed to contribute a total of 10 billion euro toward the bank bailout, Cyprus’ government is to cover the remainder – 5.8 billion euro through a one-off tax on bank deposits and 1.4 billion euro from privatisation and an increase in the corporate income tax rate to 12.5% from 10%. Interestingly, the bailout is roughly the same size as Cyprus’ 18 billion euro GDP. And it is estimated that the full cost of the recapitalisation would push the country’s debt-to-GDP ratio to 145%, from 87% in 2012.

No doubt, the deal to bail out Cyprus has somehow averted the break-up of the eurozone, but then the whole incident certainly raises new questions about the single currency area’s future. Moreover, it clearly points towards the need for European officials to solve long-lasting problems in the banking sector.

No doubt, the deal to bail out Cyprus has somehow averted the break-up of the eurozone, but then the whole incident certainly raises new questions about the single currency area’s future. Moreover, it clearly points towards the need for European officials to solve long-lasting problems in the banking sector.

Almost all economists agree to the fact that health of the banking sector can determine the health of an economy. For instance, while financial institutions have helped Switzerland thrive, banking troubles in Ireland, Iceland, and most recently Cyprus have destabilised economic activity in those countries. After all, it’s the relationship between commercial banks and governments which is key to a healthy and sound economy, and a clear case in point is the eurozone.

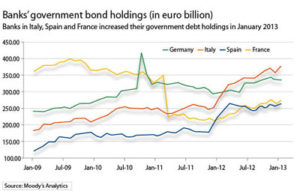

While commercial banks in Spain, France and Italy increased their government debt holdings in January 2013, it was reduced by German banks (ECB data). Although ECB does not break down which countries’ debt particular banks hold, this clearly indicates that credit institutions from fiscally troubled countries invested heavily in their own as well as other governments’ bonds. Such holdings can set up a negative relationship between sovereign risk and bank stress. A government’s fiscal problems can cause its bonds to decline in value, eroding the banks’ assets and making them more likely to require a bailout from the government, which then adds to the fiscal burden and increases sovereign risk.

In fact, this linkage can be seen in the correlation between credit-default swap (CDS) spreads for governments and banks in the eurozone’s fiscally troubled countries. While Italian and Spanish sovereign CDS spreads have moved in tandem with spreads for the major Italian and Spanish banks, CDS for Germany and its largest bank, Deutsche Bank, have moved independently, signaling that markets do not foresee the need for government assistance there.

In fact, this linkage can be seen in the correlation between credit-default swap (CDS) spreads for governments and banks in the eurozone’s fiscally troubled countries. While Italian and Spanish sovereign CDS spreads have moved in tandem with spreads for the major Italian and Spanish banks, CDS for Germany and its largest bank, Deutsche Bank, have moved independently, signaling that markets do not foresee the need for government assistance there.

Further, it’s a known fact that deposit insurance can protect a banking system, boost confidence among small savers and lessen the chance of destructive bank runs. But then, at the same time, an overly generous government guarantee can encourage banks to take excessive risks. And when insurance is paired with high deposit rates, the risk is even greater. This was exactly the case in Cyprus. Rates there on fixed-term deposits of up to two years began rising in mid-2011, even as such rates fell across the eurozone.

In fact, the spread between deposit rates in Cyprus and elsewhere in the eurozone jumped from zero in 2008 to 190 basis points in January 2013. Household deposits in Cypriot banks jumped 31% to 31.5 billion euro between 2008 and mid-2012, before falling slightly. Interestingly, at the same time bank deposits in Greece shrank by a third to 127.8 billion euro, before increasing a bit. Further, paying higher interest rates requires banks to earn higher returns, which means investing in riskier assets. Cyprus banks found these in nearby Greece, but this was a mistake. In 2012, the nation’s two biggest banks, Laiki Bank and the Bank of Cyprus, lost a combined 3.5 billion euro on Greek bonds, an amount equal to more than 20% of Cyprus’ GDP.

In fact, at the peak, Cyprus’ banks held assets roughly equal to seven times the country’s GDP, more than twice the ratio for the eurozone as a whole. Further, Cyprus wasn’t the only European banking haven. Even Luxembourg’s banks hold assets equal to more than 25 times that country’s GDP. The two other euro nations where banking sectors grew similarly oversized, Iceland and Ireland, have already experienced devastating financial crises in 2008. As in Iceland and Ireland, Cyprus’ banking system grew rapidly until it became too big to save. And it is this which really needs to stop now if policymakers want the European banking system back on track. Agrees Tomas Holinka, the Prague based Economist at Moody’s Analytics, as he tells B&E, “Eurozone banks cannot be permitted to grow larger than their home countries, and must be better funded and capitalised. If this cannot be done through negotiations, EU leaders will have to impose such regulations unilaterally.”

Although EU officials have called the Cypriot bank restructuring a special case and not a template for other troubled eurozone countries, the deal certainly serves as a model that can deter moral hazard problems across the eurozone’s banking sector. In fact, the crisis also provides an important lesson for countries that have relaxed financial regulation and lowered corporate tax rates to attract capital and foreign investment. In exchange for financial aid, the EU, IMF and ECB may now force countries to standardise bank regulation and tax policies.

No doubt, a closer integration of Europe’s banking system could help in ending the debt crisis. But then, a true banking union includes pan-European bank regulation, bank recapitalisation, and a resolution mechanism. This is only possible if ECB takes over supervision of over 6,000 financial institutions in the eurozone.

While forcing countries to harmonise their tax policies may be more difficult for the EU, with sufficient control and a lot of solidarity, this could be an important step towards fiscal union.