Dell: stake sell

Dell: stake sell

Will going private revive the PC maker’s fortunes?

Round Rock, Texas-based Dell Inc., the third-largest PC maker globally, is discussing the possibility of a potential buyout with private equity firms. Top private equity firms such as TPG Capital and Silver Lake are reportedly discussing the deal with Michael Dell, the chief executive and founder of the company who owns about 15% stake in Dell. For several years now the computer maker has been losing value and market share and has been struggling to regain its position in the PC market. The personal computer business remains Dell’s bread and butter, bringing in 70% of revenues. But as tablets, smartphones and other mobile devices have eaten away at PC sales, shares of the firm have struggled. Over the last five years, Dell’s shares have fallen by 43%, sinking into the single digits by the end of 2012.

To revive growth and cope with competition Michael Dell, who retook the CEO position in 2007, has been considering taking the company private. Dell’s enterprise value of $19.1 billion is 4.4 times earnings before interest, taxes, depreciation and amortization for the last 12 months, according to Bloomberg. That’s a lower valuation than every computer-hardware maker larger than $1 billion, except Hewlett-Packard Co, which has a multiple of 3.5, the data show. But Dell’s net cash balance of $5.15 billion provides some downside buffer as it produces opportunity for a leveraged buyout under the right conditions.

The buyout, if and when it takes place, could actually be one of the largest deals in the technology space since 2007, when KKR & Co bought First Data Corp for more than $25 billion. A buyout can be good for a company even it means investors aren’t able to trade its stocks. Entering into private ownership could amount to more maneuverability for Dell as it tries to stay afloat in a terrain full of pitfalls for PC makers.

Rio Tinto: CEO EXIT

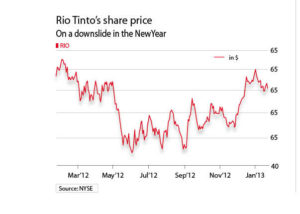

Rio Tinto: CEO EXIT

Bad bets force head honcho to quit

In the latest string of exits forced upon leaders of the world’s biggest mining companies, Tom Albanese, the CEO of the London-based minerals explorer Rio Tinto has been replaced by the company’s iron ore boss Sam Walsh. Albanese resigned over a $14bn writedown involving two of his most significant acquisitions, Mozambican coal mining and the Alcan aluminium group. The bulk of the writedown, between $10 billion and $11 billion, relates to aluminum assets acquired in 2007, while the remaining $3 billion is for Mozambique coal operations acquired only two years ago. Albanese has admitted ‘accountability’ for the loss of assets following the bad deals. Prices for metals and their ingredients have fallen sharply over the past several years with the sharp tempering of demand for mineral resources in China, Prices for coking coal have dropped 43% since 2011, when Rio Tinto made its Mozambique move. Aluminum prices have dropped 22% since 2007. At least 20 mining CEOs have stepped down in the past year under pressure from investors and boards, who blame the executives for costly mining projects that were conceived during the commodities boom.

Boeing: dreamliners’ woes

Boeing: dreamliners’ woes

787s grounded over safety concerns

After production snags and delayed deliveries Boeing’s flagship 787 Dreamliners have now run into a fresh hurdle. In recent days Dreamliners have suffered fuel leaks, a cracked cockpit window, brake problems and an electrical fire. However, it is the battery problems that have caused the most concern, leading to the grounding of all 50 Boeing 787s currently in the service of eight airlines around the world. Boeing has sold around 850 of the new planes, with 50 delivered to date. Around half of those have been in operation in Japan, but airlines in India, South America, Poland, Qatar and Ethiopia, as well as in the United States are also flying the aircraft. Meanwhile, the US Federal Aviation Administration issued a directive on Dreamliners’ airworthiness and has alerted the international aviation community. Experts say US authorities and Boeing will discuss the criteria for inspections on the Dreamliner and would also set what fixes are needed and a timetable for those. Analysts say it’s unclear how long such a process could take or how much it could cost, but some question whether Boeing can stick to its target of doubling 787 output to 10 a month by the end of this year.

Samsung: on a roll

Samsung: on a roll

Pulling in $6.6bn profit

When Apple’s iPhone 5 was launched in September 2012, analysts predicted that the handset would cross the 100-million mark in unit sales. But while Apple only managed to push out 45 million iPhones by the end of December, Samsung sold some 62 million Galaxy smartphones from October to December last year. In particular the booming sales of Galaxy S III and Note II have propelled the Korean company to again emerge as the top smartphone player in the quarter. The company also captured the biggest pie of the global smartphone market, lapping up 28% of the overall share, according to figures provided by IHS iSuppli. The former number one, Apple, managed to take a 20% grip on the market. Releasing figures for Q4 2012, Samsung said that its quarterly profit surged by 76% at $6.6 billion after the December quarter, thanks mostly to its global sales of mobile devices, memory chips, flat panels and television units.

Germany: economic headwinds

Germany: economic headwinds

Cloudy outlook for the economy

There are signs that the German economy may be slowing down. The German central bank Bundesbank, in its latest updated twice-yearly forecasts, has said there were indications that economic activity may actually fall in the final quarter of 2012 and the first quarter of 2013. After expanding by 0.5% in the first quarter of 2012, gross domestic product grew by just 0.3% in the second quarter and a mere 0.2% in the third quarter. Taking this year and next year as a whole, GDP would expand by 0.7% in 2012 and then by just 0.4% in 2013, the Bundesbank predicted. Two key factors lie behind the current slowdown. Firstly, global demand for Germany’s exports such as precision manufacturing goods and other machine tools cooled in 2012. Secondly, the economic contractions in Greece, Spain and Portugal, together with budget cutbacks and slower growth in other euro zone member states have made German firms more cautious about spending money on new plant and machinery. Should global economic growth remain below expectations or the sovereign debt crisis escalate further in euro zone countries, it is probable that the German economy may follow a much weaker course than the one now being predicted.

JAPAN: FISCAL boost

JAPAN: FISCAL boost

Massive stimulus to revive growth

Japan’s newly elected prime minister Shinzo Abe, who also served as premier back in 2006-2007, has launched a massive fiscal stimulus plan worth 20 trillion yen ($224 billion) to revive his country’s economy, which has been bearing the brunt of deflation since the past two years. The spending pledge fulfills a major campaign promise for Abe, who came to power in a landslide election in December, vowing to boost Japan’s economy and create jobs with big government spending plans. Apart from pushing up public works spending, Abe wants the Bank of Japan to take a much more aggressive monetary policy stance. These include setting a higher inflation target of 2%, focusing partially on employment on top of inflation, and actively intervening in the value of the Yen. But critics of the package also worry that public works – which form a significant portion of the measures in the plan – are doomed to be unproductive and risk creating yet more “white elephants,” alluding to infrastructure projects with no real economic value, or “bridges to nowhere,” as they were labeled during previous decades. And though Japan could indeed benefit from some post-Fukushima construction, yet concerns remain about how efficient spending in other geographic areas can be. Such spending will come at the expense of other economic sectors – including healthcare – which could genuinely benefit from more workers and investment.

Bharti Airtel: new appointments

Bharti Airtel: new appointments

Amidst ongoing restructuring, reshuffle at top

Bharti Airtel, India’s biggest telecom operator by revenue and subscribers has announced senior level organizational changes in a bid to revive its mobile business, which has been under pressure lately. Its consolidated net profit fell to 2.84 billion rupees in the third quarter ended December 31, from 10.11 billion rupees a year earlier. To stem the losses and grow its profits, the company has made some top level changes in the management. It has appointed Manoj Kohli, currently heading the firm’s international operations as its Managing Director. Bharti Airtel’s Sunil Mittal, who is currently its chairman and managing director, will become executive chairman of the company, after Kohli moves to his new role. In another major change that was announced earlier, the company appointed Gopal Vittal as its chief executive officer for India operations. The incumbent CEO Sanjay Kapoor will leave the company on February 28, making way for Vittal, who was till now in charge of special projects. Both Kohli and Vittal will report directly to Mittal. Analysts believe that the changes at the top could be because the company is looking to significantly ramp up its play in the data business. It has traditionally been strong in the voice market but now that future growth lies in data, it believes a different mindset is perhaps needed to drive this growth.

Auto: slump in sales

Auto: slump in sales

Lowest growth in nine years

The Society of Indian Automobile Manufacturers latest reports say that Indian car sales are likely to post their weakest growth in nine years this financial year. As per the industry data, the total output for the period of April-December 2012 stood at 1,697,625 vehicles as opposed to 1,677,588 in April-December 2011, a growth of just 1.19%. The overall growth in domestic sales during April-December 2012 was 4.57% over the same period last year. Passenger vehicles segment grew at 8.37% during April-December 2012 over same period last year. Passenger cars declined by -0.33%, utility vehicles grew by 59.10% and vans grew by 3.71% during April-December 2012 as compared to the same period last year. However, in December 2012 passenger car sales fell by -12.51% over December 2011. Total passenger vehicles sales also declined by -1.13% in December 2012 over same month last year.

Owing to the poor sales, SIAM will cut its car sales growth forecast for 2012-13 by 0-1%, which will effectively be its third revision for this financial year from the initial estimate of 10-12%. Anaemic economic growth, slower expansion and high interest rates, dampened sales for car manufacturers while rising fuel costs and a steeper line of credit forced many customers to defer their buying plans during 2012. Over the past few years many new car companies invested in the Indian market, riding on the back of robust economic growth till 2008. But their success was short-lived as rising car prices and increased fuel rates have scared away buyers who are majorly dependent on loan options to buy these vehicles. Sales growth registered for 2012 is a mere 2.2%, which has forced SIAM to think of new ways to bolster the market condition. Sales of home-grown players such as Tata Motors and Maruti Suzuki, which are top brands in the Indian market, have been affected while global car markers like Hyundai, GM, Ford and Nissan are also witnessing sluggish growth.

Finance: new body

Finance: new body

Commission constituted

The 14th Finance Commission has been constituted under the chairmanship of former Reserve Bank of India governor Y.V. Reddy to review the distribution of resources among the Centre, states and local bodies. The other members of the panel include M. Govinda Rao, director, National Institute of Public Finance and Policy; Sudipto Mundle, former acting chairman, National Statistical Commission; Sushma Nath, former finance secretary, and Abhijit Sen, member, Planning Commission. Sen will serve as a part time member. The Finance Commission, a constitutional body, is set up every five years and will lay down its recommendations on the sharing of tax proceeds between the Centre and the States which will apply for a five-year period beginning April 1, 2015. Among other things, it has been asked to suggest steps for pricing of public utilities in an independent manner and look into issues like disinvestment, GST compensation and sale of non-priority PSUs.

Air india: fresh hurdle

Air india: fresh hurdle

Turnaround still a distant dream

The grounding of Boeing 787 Dreamliners could not have come at a more inopportune time for Air India. For the first time since its merger with Indian Airlines, India’s national carrier had started showing signs of a revival. In November 2012, Air India made a positive Ebitda of Rs.200 million and even managed to improve its market share from 16% to 20% in the last seven to eight months. The six Dreamliners in its fleet became integral to Air India’s turnaround plan with the airline looking to expand its operations on middle-haul routes, under nine hours, to replace the ageing fleet of Boeing 777s and A-320. The Dreamliner has come to be the mainstay of AI’s plans to not only fly on long-haul routes but also cut down on costs, thanks to the fuel efficiency of the state-of-the-art aircraft. But the recent grounding of the aircraft over safety concerns has thrown a spanner in the wheel’s of AI’s future growth plans. The grounded Boeing 787s consumed 20% less fuel than competing aircraft, and their maintenance cost also came at 26% lower. So if the 787s, said to be the technologically most advanced aircraft, and considered to be the game changer for the airline, do not take to the skies at the earliest, it could mean financial implications for AI, which is struggling to work its way out of its long accumulated financial mess.

Sebi: review of regulation

Changing share buyback norms

Capital market regulator Securities and Exchange Board of India has floated a proposal to change the existing framework for buy back of shares through open market purchase. In India, companies are allowed to buy back shares through the ‘tender offer’ and ‘open market’ routes, though a majority of the purchases are through the latter route. Typically, a company announces buybacks to support its share price, boost its earnings ratios or to return surplus cash to its shareholders. Sebi has stated that there had been several instances where companies did not buy back even a single share in the 12 month offer period. Also, shares were often bought at far lower prices than the maximum buyback price announced, as there was no proper framework regarding placement of orders and periodicity. Quite often the provision to buy back shares through the open market route is just being used as a tool to manage share prices, according to Sebi. The regulator wants firms to complete their buyback offerings within three months instead of the current norm of 12 months. Also, to ensure only ‘serious players’ launch share buybacks, Sebi wants 25% of the maximum buyback amount proposed be kept in an escrow account upfront. Further, listed companies launching buyback programmes might not be allowed to raise further capital for two years and could also face restrictions on off-market deals during buybacks.

TATA GROUP: WAY FORWARD

TATA GROUP: WAY FORWARD

Cyrus Mistry’s road map for the future

Newly appointed Chairman of $100 billion Tata Group Cyrus Mistry, in his first major public announcement after assuming office, said that that group would invest more than 450 billion rupees on various businesses over the next two years and would seek to expand the group’s global presence with a focus on emerging markets in Asia, Africa and parts of Latin America. Mistry, believes that the group must differentiate itself from competitors through greater understanding of customer needs and a culture built around customer centricity, innovation and a focus on profitable growth. “We will need to be relentless in our pursuit of improving our competitiveness and in addressing the small issues that are often overlooked but end up making a significant difference in the value proposition of our products and services,” Mistry wrote in an e-mail to employees after taking charge. In his first message as Chairman of Tata Group, Mistry also said the ‘core of the Tata group’ will remain unchanged despite change in its leadership and asked the group companies to play leadership roles in their respective businesses. He also warned against any complacency, saying that history has shown that groups “that are happy with resting on their laurels are weeded out by nimble competition”.

Road projects: high profile exits

Road projects: high profile exits

GMR, GVK walk out of projects

Two of the top infrastructure firms in India, GMR and GVK groups, have pulled out of two high-profile National Highways Authority of India projects, which had a combined worth around Rs.107 billion. The two projects constitute GMR’s Rs.77 billion Kishangarh-Udaipur-Ahmedabad project in Gujarat, which it had won from the NHAI at an annual premium of Rs.6.36 billion, while the GVK project involved the Rs.30 billion Shivpuri-Dewas project in Madhya Pradesh.

The companies cancelled their contracts with the NHAI citing delays in getting forest and environmental clearances, a claim dismissed by the NHAI, which attributed the decision to the companies’ inability to secure funding. GVK needed to raise Rs.14-15 billion of equity for the Shivpuri-Dewas project, while the GMR project needed equity of nearly Rs 20 billion.

According to the NHAI Chairman R.P. Singh, the basic reason why GMR and GVK have withdrawn from the two highway projects is because these projects have become unviable due to high cost and lower toll revenue estimates. He said that concessionaires have earlier put up with environmental delays. Environment and forest clearances take anywhere between 300 days and three years and have become a major reason for projects overshooting their budgeted costs.

Also, many road projects have failed to take off because their funding has become a major issue as a result of overbidding by players. Overbidding leads to the contractor overcommiting on annuity payments to the government, leading to eventual pullouts as such projects find it hard to attain financial closure. Currently, 35 projects are awaiting financial closure because overbidding implies massive funding. The key road projects awaiting financial closure for months include those by infrastructure firms like GVK, GMR, L&T, IL&FS, Gammon, IVRCL, Essel Infra, Gayatri, Ramky, Madhucon, KNR, Soma, Sadbhav, Transstroy among others.