Too many cooks spoil the broth. Common wisdom tells us that it’s the “Too many” that is trouble. That’s precisely the problem with e-commerce in India today – “Too many”.

Too many cooks spoil the broth. Common wisdom tells us that it’s the “Too many” that is trouble. That’s precisely the problem with e-commerce in India today – “Too many”.

The last two decades have seen a complete transformation in the Indian retail landscape. A whole new generation has moved from buying groceries from nearby mom-and-pop stores to supermarkets and convenience stores. High street shopping has given way to big, swanky malls.

Now, we are witnessing another change. And this time from shopping at brick-and-mortar outlets to purchasing goods online. A busy lifestyle and the comfort & convenience that online space provides, is leading Indians to shop with their fingers.

Online shopping is still in its infancy in India. There are barriers still that prevent it from becoming popular faster than it actually is. Questions regarding credibility of merchants, doubts over quality of goods, security regarding online payment gateways, and mostly the culture-based attitude of our cash-oriented society are only a few. But all this has not deterred a host of e-commerce players in India, like Flipkart, Jabong, Myntra, Indiatimes, Snapdeal, Homeshop18, Yebhi.com and others, from wooing the Indian customer with world-class services and product offerings.

No surprise then that these players are investing heavily on product differentiation, technology, customer service and advertising.

That these players want themselves to get heard and seen is good news.

In recent months, players like Jabong, Groupon, Snapdeal, Myntra, Homeshop18 and eBay have particularly become loud about who they are and what they have to offer. A recent market report by eMarketer shows that online advertisement spending in India has grown from $0.25 billion in 2010 to $0.48 billion in 2012. Online portals are thus working hard to build brand recall. Be it online marketing through social media sites like Facebook and Twitter or improving visibility on offline vehicles like TV, Print and Radio, these e-tailers are investing big bucks in promoting themselves.

So the fight is on – differentiate, impress buyers and get cash flow positive. But that is where the problem lies. E-tailers in India haven’t still learnt the trick of making money from this much-hyped virtual shop business. A 2012 Technopak Report confirms this. The frenzy to attain a critical mass of consumers through whom they can start to make money is leading to consumer acquisition through heavy discounting (even lower than costs) and mass media advertising, resulting in very high customer acquisition costs (about Rs.1,000 to Rs.1,400 per customer as per various industry executives). Thus, to differentiate and gain consumer loyalty, e-tailers are fighting it out on the pricing front.

As such, the e-commerce business in India is increasingly become a game where the last man standing may turn out to be the biggest loser! Little wonder that this space has already witnessed consolidations. According to data compiled by Microsoft’s India Accelerator Programme, of the 379 technology product start-ups launched until October 2012, 193 were e-commerce firms, and 87 of these, including Shopveg.in, Taggle.com and Letsbuy.com, have ceased to exist. Letsbuy.com was bought by Flipkart in February 2012, while Myntra acquired Exclusively.in. Online retailers like Lensstreet.com and Dealivore.com also saw closures in 2012.

In due course of time, strategic shifts will take place in the e-commerce space, and more smaller and non-serious players will get wiped out, leaving behind clear leaders. As per Rajesh Nahar, CEO and Founder, Cbazaar.com, “E-commerce businesses in India should have a very smart balance in planning organic and inorganic growth of customer acquisition and revenue. The moment a company tries to accelerate inorganic growth by acquiring customers at a high cost and offering products at discounted rates, it will get very hard for it to get into the profitable zone.”

In due course of time, strategic shifts will take place in the e-commerce space, and more smaller and non-serious players will get wiped out, leaving behind clear leaders. As per Rajesh Nahar, CEO and Founder, Cbazaar.com, “E-commerce businesses in India should have a very smart balance in planning organic and inorganic growth of customer acquisition and revenue. The moment a company tries to accelerate inorganic growth by acquiring customers at a high cost and offering products at discounted rates, it will get very hard for it to get into the profitable zone.”

The Indian e-tailing story has also appeared very promising to investors who have bet big by investing in these start-ups. These investments have enabled players to grow and scale up quickly. Investment in the online retail space exceeded $500 million in 2011 as per VCCEdge. But the high valuation is proving to be the proverbial straw that broke the camel’s (read: e-tailers’) back as can be seen by the failure of many start-up e-tailers.

To stay alive in the business, e-tailers have already started tweaking their business models. One example of a successful e-tailer is Flipkart, that started in 2007 as an online books retailer, but extended its portfolio to media (games, music and movies) and mobile phones and accessories in 2010. In 2011, it further expanded into many other product categories such as personal care, health and home appliances. In 2012, it introduced watches, belts, bags, luggage and toys. These steps have ensured that Flipkart evolves at a steady rate and generates some diversity in revenues. Snapdeal is another player that has fast grown into a product-and-service seller. Unlike two years back when all you would have heard of in the name of Snapdeal was discount coupons for various services, today, 95% of its offering basket is filled with products! In fact, Sandeep Komaravelly, Head – Marketing & Alliances at Snapdeal.com, had an interesting challenge to throw at B&E: “Think of five weird products you could buy online and you will find at least four of them on Snapdeal. Perhaps all five.” [Our Editor tried. Komaravelly won!]

Limited availability of brands in Tier-I and II locations is driving consumers to shop online. And e-tailers are paying attention. One of them is Jabong. The company has put in place 55,000 special packaging units (as on January 2013) to ensure the shortest possible time of delivery. At present, the company offers same-day delivery only across metros. In 2013, tier II cities would enjoy the facility. And by 2015, expect the company to replicate the same across tier III towns. Says Manu Jain, MD, Jabong.com, to B&E, “In 2013, we will ensure that we follow the same day delivery concept in tier II cities as currently, in those locations we have a next day delivery system. We will also be focusing on minimising the time involved in resolving customer problems as well.”

E-tailers are experimenting with new methods to engage end-consumers. Trends like cash-on-delivery (COD), replacement of goods if found unsuitable, delivery-post-trial et al are on a rise. States Sharat Dhall, President, Yatra.com, “We have made significant brand investments to build the brand and drive consumer trial, while at the same time, we have invested aggressively in consumer-friendly processes to ensure that consumer experience is an excellent one, driving long term loyalty and retention.” This fight against brick-and-mortar has become loud already. But the traditional retail format is not going anywhere soon. Think of the challenges that online companies face and you’d understand why. India has over 6500 e-commerce companies and most of them are struggling with problems relating to payment options, logistics, infrastructure and consumer service. An e-tailer can tempt a consumer once, but if the erosion of trust starts from the very delivery stage, that particular e-commerce brand can expect little in the name of good-word-of-mouth marketing.

E-tailers are experimenting with new methods to engage end-consumers. Trends like cash-on-delivery (COD), replacement of goods if found unsuitable, delivery-post-trial et al are on a rise. States Sharat Dhall, President, Yatra.com, “We have made significant brand investments to build the brand and drive consumer trial, while at the same time, we have invested aggressively in consumer-friendly processes to ensure that consumer experience is an excellent one, driving long term loyalty and retention.” This fight against brick-and-mortar has become loud already. But the traditional retail format is not going anywhere soon. Think of the challenges that online companies face and you’d understand why. India has over 6500 e-commerce companies and most of them are struggling with problems relating to payment options, logistics, infrastructure and consumer service. An e-tailer can tempt a consumer once, but if the erosion of trust starts from the very delivery stage, that particular e-commerce brand can expect little in the name of good-word-of-mouth marketing.

Payment security is another concern for online buyers. Internet security and payment facilities have to be made foolproof else fraudulent activities can compromise the security of e-tailing websites.

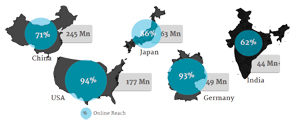

So there are challenges. But good news for sellers is that critical mass has been reached. Today, the count of Internet users stands at 139 million (as per comScore; December 2012), a count that is set to rise by 137% to 330 million by 2015 (as per McKinsey & Company). So how big are the potential revenues? As per McKinsey, this could translate into $34 billion in toplines earned by Internet portals in India by 2015 (in 2012, they made $14 billion). Care has to be taken to convert a big proportion of the additional topline to profits while maximising buyer satisfaction, overcoming bottlenecks and investing in clutter-breaking brand recall exercises. It’s more difficult than booking cineplex tickets online; actually, many times over!

Amazon began in 1995, but it only entered the profitable zone six years later. One of the first successful online companies in India Flipkart that started in 2007 may turn tables by the time 2013 ends. And this year, might be the end of the loss-making patch for others like Groupon.com, Snapdeal.com and Myntra.com in the Indian market. That was hope.

Here’s reality. Today, the cost of acquiring a new customer is 150%-400% more than the average price of a book sold on Flipkart. Get the drift?