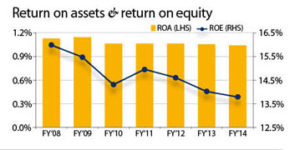

Capital norms: A problem

Capital norms: A problem

Annual return on equity for Indian banks has constantly declined over the past few years. While the figure was at 16% in financial year 2007-08, it is now expected to touch 14% in FY’14. Similarly, RoA for Indian banks, which was close to 1.2% in FY’08, has now come down nominally over the past few years. Prime reasons for this is the increase in mandatory capital levels. This has left the banks with comparatively lesser money to lend.

Banks may turn back at customers

Banks may turn back at customers

While most banks have decided to pass on the benefit of the interest rate cuts to their customers in the past, this may not happen again. This time, the banks may focus on preserving net interest margin (NIM) by maintaining their base lending rates. This simply means that even if the RBI reduces policy rates, the benefits may not reach the end customers the way it should have.

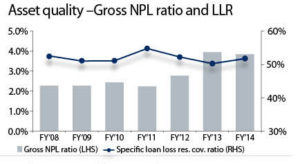

Asset quality to improve gradually

Asset quality to improve gradually

Deterioration in asset quality for the Indian banks may finally come to a halt in the coming financial year. However, this improvement may not be very sharp considering that many companies are still planing to raise financial leverage for their projects in the next financial year. Nevertheless, the cyclical up-trend is likely to provide a much needed respite from further deterioration of asset quality and may help begin a gradual recovery.

B&E IndicatorsCaution mixed with aggression

B&E IndicatorsCaution mixed with aggression

Standalone financial reports of 334 companies with a debt burden of over Rs.5 billion (excluding oil marketing companies) suggest that the net profit margin as well as interest coverage ratio of these companies have been consistently deteriorating. This creates an alarming situation for the lenders as the risk of substantial amounts of loan turning “dead assets” goes up. Banks need to be sufficiently cautious on the same.