Not many know about the historical “drop-test” that the iPhone had failed when it was launched. It is a different matter that the test – where the iPhone was dropped from a height of 5 feet on concrete at many angles – was conducted by a group of scientists at Nokia’s R&D labs. Nokia’s engineers did a lot of research with the iPhone when it was first launched six years back. They declared the new generation smartphone unfit for new generation (3G) technology, delicate for daily usage, and expensive to manufacture. In a quick line – Nokia’s technology masters weren’t amused by Apple’s creation, and were quick to declare that neither would consumers be happy with the technology or design of the iPhone nor would the very company that created it.

Not many know about the historical “drop-test” that the iPhone had failed when it was launched. It is a different matter that the test – where the iPhone was dropped from a height of 5 feet on concrete at many angles – was conducted by a group of scientists at Nokia’s R&D labs. Nokia’s engineers did a lot of research with the iPhone when it was first launched six years back. They declared the new generation smartphone unfit for new generation (3G) technology, delicate for daily usage, and expensive to manufacture. In a quick line – Nokia’s technology masters weren’t amused by Apple’s creation, and were quick to declare that neither would consumers be happy with the technology or design of the iPhone nor would the very company that created it.

A year later, the iPhone 3G was made ready, and Tim Cook is a living example of how supply chain can help bring costs down and enable a new technology to be sold at high margins. That Apple’s smartphone would prove a dud turned a case of wishful thinking for Nokia. Consumers on the other hand, had evolved from desiring bulky, unbreakable hardware to demanding complex software sandwiched between delicate front and back designs that made the product look appealing.

That its engineers realised the potential of Apple’s smartphone revolutionising technology only a year after it was launched isn’t the only regret Nokia has today. More than seven years before the iPhone was launched or a decade before the Samsungs and HTCs took the world by storm with their devices that lured modern technology lovers, the research and design team at Nokia (headed by the-then chief of design Frank Nuovo) actually gave presentations to educate wireless carriers and investors about what the smartphones of tomorrow would be. They revealed plans for a phone that had a colour touchscreen and a single button on the front, and was capable of locating restaurants and order lipstick. In fact, Nokia’s engineers had developed a much-before-time touchscreen tablet in the late 1990s that boasted of being able to function through a wireless connection. Think about it – these are the very identification points of what today’s successful smartphone makers roll out in the names of phone, tablets and phablets. For Nokia however, the realisation dawned on it too late. The lesson was learnt, but much after it found itself gasping for breath in an ever-increasing clutter.

Much as it would be a case of waking up the near-dead, Nokia’s dealings in the smartphone market have been one that would have oracles confused. After Jorma Ollila took over as CEO in 1992, the company did start betting on the next wave in telephony. It spent billions of years each year on R&D to boost its telecommunications business. Think of the world’s first real well-marketed smartphone and the Communicator (the Nokia 9000) would be right up there. That was in 1996. Though it weighted about a pound, it was the world’s first mobile handset that offered email, fax and online surfing on a single hardware piece. It was a technology that didn’t have buyers shelling out money on in 1996, but in the early 2000s, with incremental innovation on design and OS, would have found buyers in the millions. Clearly, Nokia was then about 5 years ahead of other phone makers.

It failed to capitalise on the magic touch found early.

It failed to capitalise on the magic touch found early.

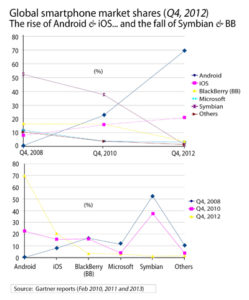

From a high of over 70% a decade back, today, its global market share is under 20% (19.1%; FY2012; source: Gartner February 2013 report). The advent of Motorola killed any chance of it becoming the ‘leader forever’. That forced the first error that sparked-off Nokia’s transition from a smartphone manufacturer to a dumbphone maker. In 2004, when Motorola’s Razr flip-phones became a hit, investors started blaming Nokia’s management and R&D teams for spending billions (it spent about $40 billion on R&D in the decade leading to 2010) on researching breakthroughs in mobile email, touch screens and wireless networks. The blame was that the Finnish manufacturer was wasting its efforts on high-end, expensive smartphones, while rivals like Motorola, Samsung and LG grabbed its lucrative market of inexpensive dumbphones around the world. Bad luck – that was precisely the time when the wall dividing consumer technology in enterprise and mobile communications was crumbling. After Olli-Pekka Kallasvuo, took over as CEO in 2006, to please investors and the management, he merged the company’s smartphone and basic-phone operations. Outcome – the more profitable dumbphone business gained importance, and Nokia’s march into the world of smartphones stalled.

Some claim that for Nokia, its effort to blend smartphones with dumbphones was a result of it entering the smartphone market too early. Agreed. But of the $40 billion it spent between 2000 and 2010 on R&D, if only a billion or two had been diverted to preserve its smartphone prowess and continue working on technology (both software and hardware) for the next decade, Nokia wouldn’t have been what we call today – a smartphone maker turned dumb!

The second mistake Nokia made was that it failed to evolve on the Operating Software front. And this is where handset makers like Apple, Samsung, HTC and others have thrived (compare the experience on a Symbian or a MeeGo versus that on an iOS or Android and you get the drift). While one R&D team worked hard to revamp Symbian OS – a bug-laden aging OS that had become obsolete by the time Kallasvuo took over and was running most of its smartphones, another working on the now-history MeeGo was trying to win capital and management attention to destroy Symbian. Result was – none managed to impress buyers in the second half of the 2000s, and only exposed Nokia’s convoluted management structure. Several years had elapsed before Nokia realised that buyers’ requirements had evolved beyond its basic Symbian OS. It then scrapped its Symbian project in a hurry, and sided with the Windows OS platform in 2011 to power its smartphones. But again, that combine is yet to prove its mettle. The third mistake on Nokia’s part was its failure to create a coherent application ecosystem – a must for smartphone makers. Though Nokia was the first to bring downloadable and third party applications on its phones on the Java and Symbian C++ platforms, its ecosystem remained largely unfragmented. Also, for those willing to experiment with discovering, purchasing and installing third party apps, the experience was prehistoric. Much blame for failing to upgrade its technology goes to the lack of a proper model that enabled distribution of applications. Its largely fragmented design and device hardware models that supported new age softwares upset high-end users who parted ways in the second half of the last decade and jumped ship to using iPhones and Android-powered phones that offered a huge app market and an engaging UI interface – a costly mistake for a company that accounted for 30% of the mobile phone industry’s R&D spend in the past decade (Bernstein research 2010). Mistake number four was that it lost focus on providing seamless Internet services (that consumers loved ten years back and still do) and got blindfolded by its services ambition. One big reason for this was Nokia’s obsession with emerging markets where Internet services are still what you would term ‘third-world’. This blind spot made Nokia focus more on services like maps and geo-tagging and trying to create its own social network, instead of leveraging what third-parties – like Facebook and Twitter – had to offer on a platter. An expensive acquisition like the $8 billion buyout of Navteq was a result of this myopia. What Nokia represents today is a typical case of ‘innovator’s dilemma’. It went ahead with what it thought the market liked and therefore lost billions (and a future), rather than risking little by trying to experiment with what the market could have liked. The world of apps that Android and iOS have made famous is an example of how companies like Apple and Samsung have avoided this dilemma.

The second mistake Nokia made was that it failed to evolve on the Operating Software front. And this is where handset makers like Apple, Samsung, HTC and others have thrived (compare the experience on a Symbian or a MeeGo versus that on an iOS or Android and you get the drift). While one R&D team worked hard to revamp Symbian OS – a bug-laden aging OS that had become obsolete by the time Kallasvuo took over and was running most of its smartphones, another working on the now-history MeeGo was trying to win capital and management attention to destroy Symbian. Result was – none managed to impress buyers in the second half of the 2000s, and only exposed Nokia’s convoluted management structure. Several years had elapsed before Nokia realised that buyers’ requirements had evolved beyond its basic Symbian OS. It then scrapped its Symbian project in a hurry, and sided with the Windows OS platform in 2011 to power its smartphones. But again, that combine is yet to prove its mettle. The third mistake on Nokia’s part was its failure to create a coherent application ecosystem – a must for smartphone makers. Though Nokia was the first to bring downloadable and third party applications on its phones on the Java and Symbian C++ platforms, its ecosystem remained largely unfragmented. Also, for those willing to experiment with discovering, purchasing and installing third party apps, the experience was prehistoric. Much blame for failing to upgrade its technology goes to the lack of a proper model that enabled distribution of applications. Its largely fragmented design and device hardware models that supported new age softwares upset high-end users who parted ways in the second half of the last decade and jumped ship to using iPhones and Android-powered phones that offered a huge app market and an engaging UI interface – a costly mistake for a company that accounted for 30% of the mobile phone industry’s R&D spend in the past decade (Bernstein research 2010). Mistake number four was that it lost focus on providing seamless Internet services (that consumers loved ten years back and still do) and got blindfolded by its services ambition. One big reason for this was Nokia’s obsession with emerging markets where Internet services are still what you would term ‘third-world’. This blind spot made Nokia focus more on services like maps and geo-tagging and trying to create its own social network, instead of leveraging what third-parties – like Facebook and Twitter – had to offer on a platter. An expensive acquisition like the $8 billion buyout of Navteq was a result of this myopia. What Nokia represents today is a typical case of ‘innovator’s dilemma’. It went ahead with what it thought the market liked and therefore lost billions (and a future), rather than risking little by trying to experiment with what the market could have liked. The world of apps that Android and iOS have made famous is an example of how companies like Apple and Samsung have avoided this dilemma.

The last mistake was Nokia’s misunderstanding of the volatility of its brand strength. It overlooked the potential of its emerging competitors and assumed that consumers would side with it no matter what.

That didn’t happen.

Talking on Nokia’s recent financial announcements, London-based Michael Dunning, MD of Fitch Ratings tells B&E, “The troubles facing Nokia were highlighted by its announcement that its Q2, 2012 devices and services operating margin will be less than negative 3%. This will lead to a precarious combination of a depleted cash balance without an end in sight to the declining cash flows. Given the strategic challenges facing the company, these trends are not particularly surprising. The company needs to return to generating positive operational cash flow.”

If this Finnish major was a casualty from the mid-2000s, there is a Canadian smartphone maker who has been a symbol of failure in recent times. BlackBerry. It has wobbled in the past three years. Its market share has been falling and is today down to 3.5% in the smartphone category (in FY2012, from a high of 20% in 2009; Gartner 2013 report). It is largely viewed as a compromise-seeking survivor and has launched two new handsets (Z10 and G10) and a new OS (BB 10) to win back fame. After the mistakes it made under the leadership of former Co-CEOs, this one sounds a difficult proposition. No surprise it has been that in over 13 months since Thorsten Heins became the technology major’s CEO, only once has he got the opportunity to dance onstage to announce a new launch.

Ten years back, BlackBerry had begun a run as the new destination for enterprise mobility solutions and hardware. In the years that followed, up until 2009, it became a common noun amongst customers in the retail segment. But the iPhones and Androids have made its products look clunky – its hardware and OS have been below par with no suitable upgrades or design changes made to answer competitors’ challenges. The influx of iOS and Android consumer-focused devices brought into enterprises by employees and the inability of BlackBerry to meet user – rather than business – concerns, have hurt it.

BlackBerry’s first mistake was that it failed to upgrade with time its software catalogue and hardware independence to remain attractive to the home consumer. BB 10 represents the company’s attempt to reduce this gap, but it is too little, too late. Even when iOS and Android started evolving as non-closed platforms, and it became clear that BlackBerry would now have to compete with Windows OS, it continued to work on developing an innovated version of a software around the QNX software. Problem was – QNX was not originally made for smartphones. It was developed as an embedded OS for entertainment systems in the auto industry. On the app front, while Apple stood to gain in the consumer market by being the first to offer devices that were supported by an extensive software library, Android was able to keep pace with the change due to its open source architecture. Talking of apps, the BlackBerry online store only has 70,000 at present – too few as compared to the iStore’s count of 775,000+ and Android’s 750,000+. Even developers are not too excited when it comes to making apps for BlackBerry. As per IDC, developer interest in the BB 7 and BB 10 platforms have fallen to 9% from 27% (June 2011). In comparison, developer traction for Windows has continued to rise for the past 12 months and today stands at 38%, while that for iOS is 90% and Android OS is 76%. Enterprise app developers are not so excited about the BB 10 either. As per IDC, iOS and Android remain the top two platforms for enterprises. For BB, this number is only 10% for smartphones.

The app development exercise on the enterprise front is critical for the company if it is to have a chance to survive for some years as Colorado-based Steve Brasen, Managing Research Director, Enterprise Management Associates, tells B&E, “There’s a certain irony in the fact that RIM’s key target audience should be the enterprise market that it neglected when it finally recognised the importance of consumerisation.”

While adding meaning to how BlackBerry has become a smartphone maker turned dumb (and fast vanishing), experts predict that this now dumbphone maker’s distress signal is getting louder. Speaking to B&E, Achal Sultania, a London-based Credit Suisse analyst forecasts, “We see a prolonged period of losses ahead for BlackBerry. This means, even after a brief return to break even, the company cannot avoid moving to an accelerated period of losses with commensurate cash burn.”

The second mistake that BlackBerry has made is that it has changed its services model. The transition to the next generation platform will force a change in its services business, which will only further cause profit margins for the smartphone and tablet-maker to deteriorate. BB10 (unlike the previous versions, and like the Playbook based upon the QNX that did not leverage the Network Operating Centre, NOC, infrastructure at all and relied upon Microsoft Active Sync) will not utilise the NOC-based architecture. This will reduce ARPU levels on the BB 10 platform. BB 10 products will not be integrated with the network infrastructure in a way that previous products were. Especially to make the best use of the ‘balance’ feature that BB 10 provides, enterprises would have to deploy a BlackBerry Enterprise Server (BES 10). This may discourage many enterprises that have already moved away from BlackBerry or are planning to do so in the near term, thereby reducing its market power. While speaking to B&E, Mathew Cabral, a New York-based Credit Suisse Analyst says, “We see BB shipping some 15-17 million BB10 devices in FY 2014-15, which gives it a smartphone share of only 1-2%. The portfolio is aimed at the high end (above $400) and will struggle against two formidable competitors of Apple and Samsung given the company’s weaker portfolio.” Conclusion: the subscriber base of BlackBerry will decline going forward.

The third mistake that BlackBerry made was that it abandoned its primary cash cow for a highly unsuccessful product – the Playbook tablet. At the same time, it lost focus on who its customer was. For close to two years, the company set aside development work on its smartphones and diverted lab and marketing resources and innovation to its tablet development project. As such, the company even forgot to market its smartphone well. The outcome was tragic. Not only is the Playbook written off as an outright failure, the company has even lost grace in the smartphone market.Because the company ignored its smartphone hardware and OS businesses for a couple of years, its customers (and the world of smartphone buyers) are today ignoring it loudly. What also worsened this mistake was the confused perception of BlackBerry’s management over who its customer was. While its former co-CEO Mike Lazaridis was in favour of the enterprise market, co-CEO Jim Balsille fought hard to bring BlackBerry products to retail consumers. This mistake of diverting focus and resources to the wrong product and massive confusion over target market resulted in mixed branding and PR efforts, thereby reducing BlackBerry to a dumb, clunky phone-making brand. BlackBerry made headlines in 2006 for the right reasons. Today, its epitaph is talked about. Consumers today find no incentive in what BlackBerry has to offer.

There are two lessons that this tale of two smartphones makers turned dumb has to teach us.

First, technology that consumers love is everything. Look at the iPhone. Look at the the Android OS and how Samsung and HTC have leveraged this platform. These are examples of companies which have gone the “win the consumers” way. Unlike Nokia and BlackBerry who decided that consumers would come to them no matter what, these companies have gone the distance, experimenting, failing and losing some revenues and market value but beating analyst estimates and selling record number of handsets each passing year. Second, one blockbuster of an idea and product innovation isn’t enough to give thorns to competition. Innovative miracles – whether they come at the cost of spending R&D budgets or buying out technologies – will only continue to make a technological company more adaptive to changing consumer tastes and evolving technologies.

Both Nokia and BlackBerry have learnt their lessons. Only regret is – they may not live long enough to prove that they have found a way to crawl out of the dry well of innovation. Consumers on the other hand will continue to forget bygones and spend their earnings on the smartphone maker that gives them a new world to experience with each time.

Steven Philip Warner, editor, business & economy