")

Slowing demand

Slowing demand

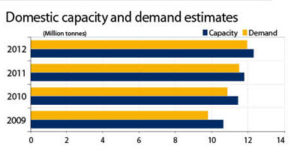

Overall paper demand from all segments is expected to remain tepid in 2013 due to a weak economic outlook on both domestic as well as international front. The domestic demand went down by about 4% in 2012 as compared to sluggish 6% growth in 2011. The industry had reported a phenomenal jump of 13.9% and 10.2% in 2009 and 2010 respectively. However, it is likely to bounce back by 2013-end due to significant capacity addition and lower prices.

Backward integration is the key

Backward integration is the key

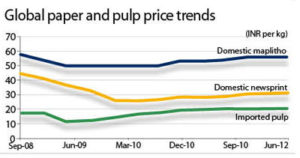

Global pulp prices went down moderately in 2012 as compared to 2011. Yet a significant depreciation in the value of rupee didn’t allow the domestic manufacturers to get benefited from this. To fight out volatility in the international market, domestic manufacturers have resorted to backward integration in the last few years. But, they still continue to import some specialized grades of pulp.

Power crunch

Power crunch

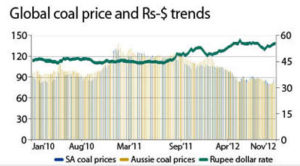

Inconsistent domestic coal supplies forced the manufacturers to remain heavily dependent upon imports. Here too, a weak domestic currency added to the woes of high costs. Both these issues are not expected to be settled in the near future. Hence, the operating profitability of paper companies would remain under pressure in the 2013. However, an expected increase in sales volumes may provide some much needed support.

Sticky margins

Sticky margins

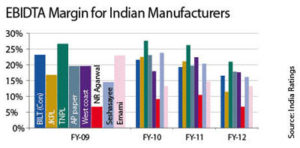

Recently, the industry faced serious pressures on the margins front due to high input costs. Further, the capacity addition in the WPP and paperback segment has pushed the inventories for these manufacturers. These inventories will take some time to get absorbed. The whole situation is putting pressure on prices. Hence, the companies will have a tough time in the short run but the long term remains a safe or perhaps a fruitful bet.